This piece was originally published in International Aquafeed Magazine - August 2021

Listening into some of the recent proliferation of webinars, my attention was drawn to two presentations by different feed companies, where the message could have been one of almost mimicry of each other. Both presentations were excellent and the harmonisation in each of the stories being told had a kind of comforting feel to it. Each presentation told the story of how each company’s raw material portfolio had changed over time but also where they each thought the future might take their respective companies.

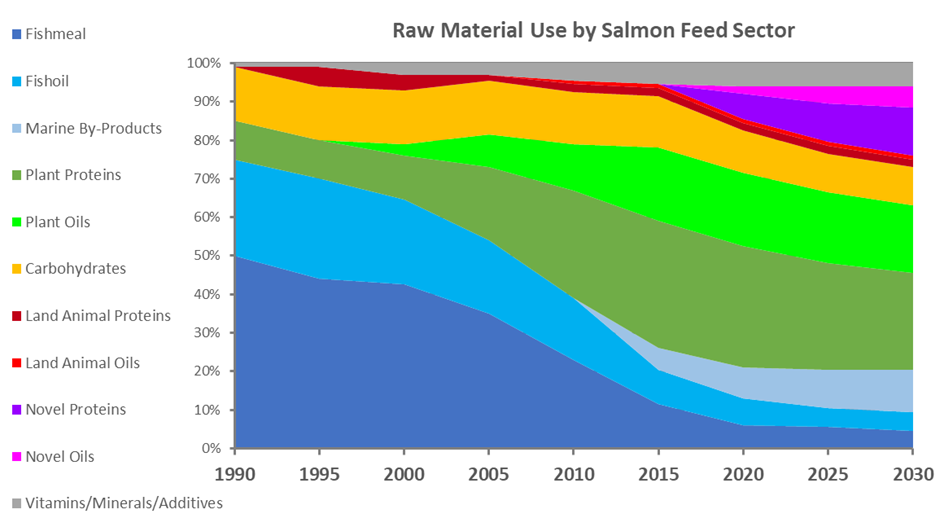

Each story presented how in the origins of feed (salmon feed for the time being) raw material use, that it was mainly the marine resources (fishmeal and oil) that were used in the 1990’s (Figure 1). Early forays into “alternative ingredients” explored (briefly) animal proteins and plant proteins, the latter of which progressively increased in use till 2020, with the former being phased out for various reasons before 2005. Notably, around 2020 the use of fishmeal and other marine proteins appeared to have “bottomed out”. As for oils, while the origins were strongly with fishoil, in the mid 1990’s the use of plant oils began, and this increasingly replaced fish oils such that by 2020 close to 75% of the oil used was not of marine origin anymore. By 2020 we also see that there is significant reliance on eight resource streams compared to four in 1990. In essence, what we were seeing was an evolution of feed formulations based on simplicity towards one of complexity.

In 2020 some other interesting changes were notable. Novel proteins were now being included in feeds at levels equal to fishmeal. The use of “circular” protein and lipids was also emerging, notably the use of fishmeal and oil from trimmings and by-products. In fact, this sector emerges as one of the more notable resources moving forward. Further of note was that the level of marine ingredient use (whether forage origin or trimmings) was also flat lined going forward. The importance of using marine ingredients from certified sources was also highlighted as important in moving forward. The other important observation made by the presenters was the change in impacts associated with these changing strategies.

Interestingly, the original marine ingredient focussed strategy was one that in reflection had a pretty good environmental footprint; low CO2 discharge, low energy use, and little to no reliance on land or freshwater. Compare that with the modern approach which had a comparatively high demand for energy, high CO2 footprint and used substantially more land and freshwater. Even the new novel resources-on the-block were indicated as being not so great in their footprints but did provide increased resource security and reduced contaminant issues. They also brought in new nutrients as options in a situation where there is growing demands on the existing resources.

So, if in a sustainability context we are not better off in 2020 than 1990, why did we change you might ask? Well, that question goes back to the original reason we began using “alternatives” in the first place, which was based on the recognition of constraints to expanding the availability of marine ingredients as aquaculture feed demand grew. It wasn’t that we considered the marine ingredients bad or unsustainable, but rather that there was simply never going to be enough of them. We had to “add new things to the dinner table to accommodate the increasing number of mouths to feed”. A review the data presented shows that these companies had clearly thought about that very issue – what to feed those new mouths. Their answer not surprisingly was more novel ingredients + more marine by-products, but less plant proteins. It seems the future for the feed sector is one of a two-pronged approach with both increasing circularity in resource use plus coupled with new novel tech to bring additional resources to the table.

Figure 1. A summarised representation of the percentage raw material usage by major salmon feed manufacturers from 1990 to 2030, showing the change in resource focus and shift from simplicity to complexity.

Author: Dr Brett Glencross, July 2021